The Cost of Constant Crisis

How America lost the discipline to govern its own economy, and why the math may soon make the decision for it.

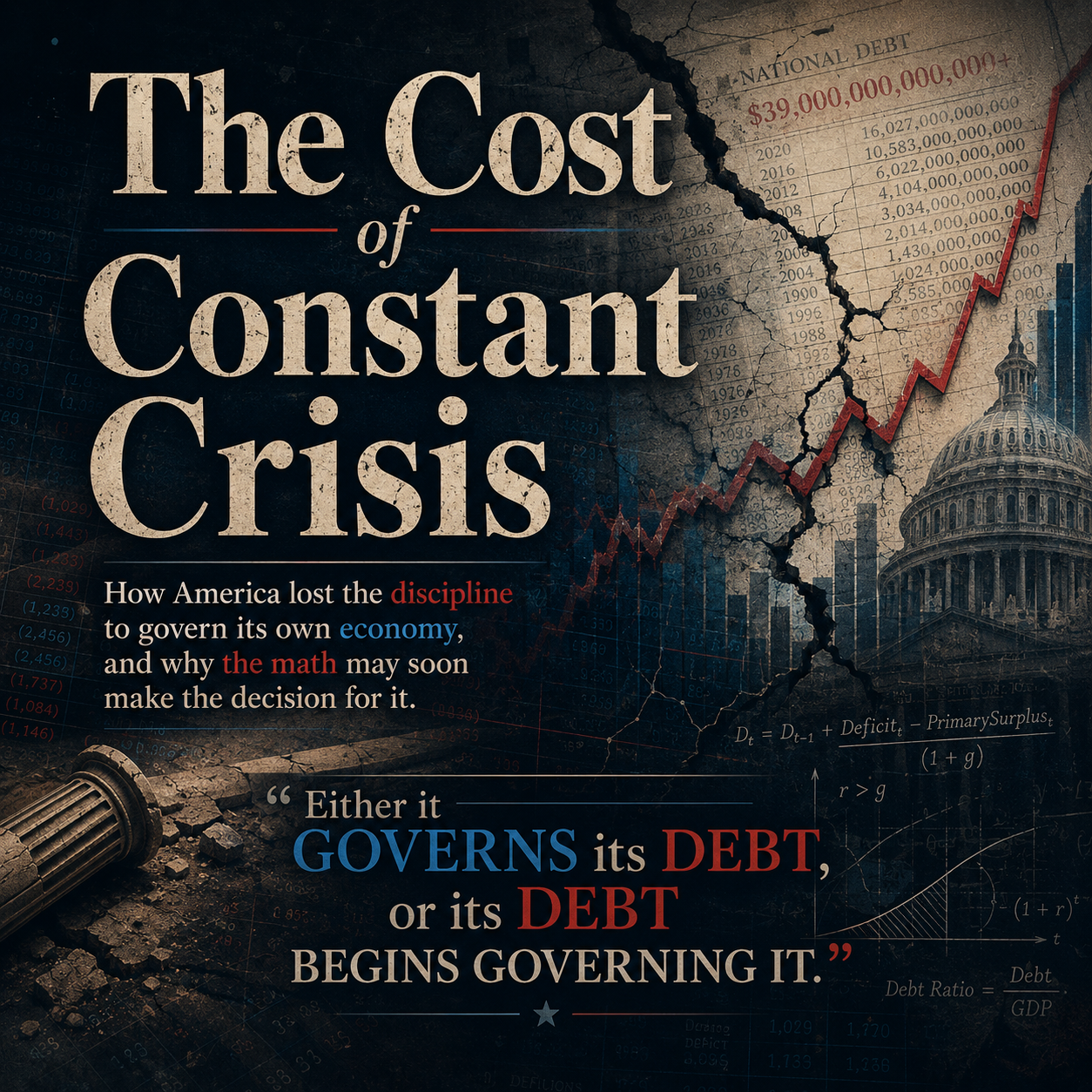

"The instability Americans feel today was constructed slowly, across decades and across parties, by leaders who discovered that borrowing was politically easier than choosing."

By Billy J Bailey

There is a phrase Americans have heard so often it has lost whatever meaning it once carried: “It has to get worse before it gets better.”

Politicians reach for it when prices rise, when markets lurch, when gasoline spikes, when borrowing costs climb beyond what ordinary households can absorb. The phrase is designed to sound responsible. Mature. Strategic. Like someone in charge has thought through the pain and decided it is necessary. Increasingly, it sounds like an excuse. After years of inflation, expanding debt, and political dysfunction, Americans are beginning to ask a harder set of questions: What if things are not getting worse because leaders are making difficult but necessary choices? What if things are getting worse because Washington has lost the capacity, or the will, to govern responsibly at all?

Those questions belongs to no single party. One of the most durable myths in American political life is the assumption that the country’s economic troubles began with the last administration, whichever one that happens to be. They did not. The instability Americans feel today was constructed slowly, across decades and across parties, by leaders who discovered that borrowing was politically easier than choosing. That discovery, repeated often enough, became a reflex. The reflex became a system. And the system is now visibly straining.

In 1970, the federal deficit stood at $3 billion. By 1975, it had climbed to $53 billion. During the Reagan years, deficits surged past $200 billion as tax cuts, military expansion, and domestic spending grew in tandem. By the early 1990s, annual deficits were approaching $300 billion, and a growing number of Americans had begun to suspect that Washington had permanently lost control of the nation’s finances. That suspicion created space for an unlikely political figure.

Ross Perot’s 1992 presidential campaign was, by the standards of professional politics, almost comically unpolished. He was blunt, unconventional, and constitutionally incapable of the kind of smooth reassurance voters had come to expect from national candidates. But he had identified something the political class preferred not to discuss directly: the national debt was not a technical problem waiting for a technical solution. It was a symptom of a governing class that had decided avoiding hard choices was preferable to making them.

Political insiders mocked him. His charts became late-night material. He received not a single electoral vote. He did, however, receive 19 percent of the popular vote, the strongest third-party showing since Theodore Roosevelt’s third term attempt, because millions of Americans recognized that his warnings were grounded in something real. At the time, the national debt stood at approximately $4 trillion. Today, it exceeds $39 trillion.

For a brief, genuinely remarkable moment, Washington appeared to absorb the lesson. The Clinton administration and a Republican Congress, shaped in part by the fiscal urgency that figures like John Kasich brought to the budget process, managed to balance the federal budget. The government posted surpluses in 1998, 1999, 2000, and 2001, the first sustained surpluses since 1969. The achievement was real, and its significance extended beyond the numbers. It demonstrated that fiscal discipline was not a fantasy. It required compromise, prioritization, and a willingness to think past the next election. All of those things, it turned out, were possible. None of them proved durable.

The wars following September 11, successive rounds of tax cuts, and the catastrophic financial collapse of 2008 pushed deficits sharply upward again. By 2009, the annual deficit exceeded $1.4 trillion. Barack Obama inherited the worst economic crisis since the Depression, and emergency intervention was not optional. But the scale of the response permanently altered something in the political culture surrounding debt. Trillion-dollar deficits stopped feeling like emergencies and started feeling like baselines.

Mitt Romney tried to make that normalization the center of his 2012 campaign. With the debt just above $16 trillion, he argued with some persistence that a country unable to govern its finances would eventually lose the flexibility to govern much else. The argument was dismissed as the predictable concern of a fiscal conservative in a recovering economy.

The debt has more than doubled since then. Washington now discusses it with less urgency than it did when Romney was raising the alarm. That trajectory, more than any single policy decision, captures what has actually changed: not the numbers, but the seriousness with which the political class is willing to engage them.

Donald Trump entered office in 2017 inheriting a stable economy. Unemployment had declined steadily for years. Inflation was contained. Consumer confidence was solid. What followed was, among other things, a case study in what happens when a government conflates economic performance with economic stewardship. Stock market levels became the primary metric of success, cited with a frequency that suggested the administration understood the market less as an indicator of economic health than as a daily referendum on presidential competence. Growth became branding.

The underlying structural pressures, including a debt trajectory that was accelerating even before the pandemic, received comparatively little attention. Deficits climbed from $585 billion in 2016 to nearly $1 trillion by 2019, during a period of relative prosperity when the conventional logic of countercyclical fiscal policy would have argued for restraint. Trump had spoken in his first campaign about eliminating the national debt within eight years. The direction of travel was precisely the opposite.

When the pandemic arrived, the emergency was genuine and the federal response was, in important respects, necessary. Millions of Americans needed direct support. The alternative, allowing widespread business failure and household collapse during a public health crisis, was not a serious option. But the design of the response carried consequences that Washington has been reluctant to fully account for.

Enhanced unemployment benefits, adding $600 per week to standard payments, provided meaningful relief in the immediate term. They also reset wage expectations across large segments of the labor market in ways that proved difficult to reverse. Jobs that had paid $9 or $10 an hour could no longer attract workers at those wages. Some of that shift reflected long-overdue correction in a labor market that had chronically undervalued certain kinds of work. But when wages rise faster than productivity, businesses absorb the difference through prices.

When simultaneous supply chain disruptions removed the usual pressure release valves, the result was an inflation surge that caught the administration, and much of the economics profession, unprepared. The governing instinct throughout remained oriented toward the news cycle rather than the balance sheet. That preference would cost the country considerably more than it appeared to at the time.

Joe Biden inherited an economy running too hot, with pandemic-era stimulus still working through the system and inflation beginning its ascent. What the moment called for was visible, credible leadership focused on stabilization and restoration of confidence. What it frequently got was an administration that seemed genuinely uncertain about the gap between its economic narrative and the experience of the people it was describing. The White House cited macroeconomic indicators that were, by conventional measures, encouraging. Unemployment remained low. GDP growth was positive. The administration pointed to these figures with evident pride.

Meanwhile, grocery bills climbed. Insurance premiums rose. Housing, already strained before the pandemic, became unaffordable across markets that had previously been accessible to middle-income families. Mortgage rates, responding to the Federal Reserve’s belated efforts to contain inflation, made the prospect of homeownership remote for a generation of younger Americans. People do not experience the economy through quarterly reports. They experience it through the specific, concrete transactions that structure their daily lives. The administration’s apparent difficulty grasping that distinction became, over time, its defining political liability.

By 2024, the gap had hardened into something no amount of messaging could close. When Biden’s exit from the race became unavoidable, the Democratic Party’s response revealed its own institutional limitations. Kamala Harris secured the nomination without a contested primary, without a single vote cast for her presidential candidacy in the 2024 cycle. The process was defensible under party rules. It was legible to voters primarily as a party protecting its own interests under pressure. And Harris faced a challenge that no candidate in that position could have easily navigated: she could neither fully own an economic record that voters had already passed judgment on, nor credibly separate herself from it.

Trump, running his third campaign, understood the electorate’s mood with the kind of intuition that is often mistaken for strategy. Exhausted voters do not primarily want policy nuance. They want someone who appears to grasp that things are wrong and is willing to say so directly. His return to the White House was not a verdict on his first term’s economic record. It was a verdict on an incumbent party that had spent four years telling people their lives were better than they felt.

In his second term, Trump has continued applying the same framework to a different set of circumstances, with predictable results. The administration has pressed the Federal Reserve to lower interest rates, a preference that reflects a consistent governing instinct: whatever produces near-term visible improvement is preferable to whatever might produce lasting stability. Lower rates make borrowing cheaper, stimulate activity in rate-sensitive sectors like housing, and tend to produce short-term market appreciation. They also, when deployed alongside structural deficits of the scale the United States is currently running, risk reigniting inflation and further eroding the dollar’s credibility as a store of value.

The logic is familiar from household finance. Reducing the interest rate on your debt does not solve a debt problem if you continue adding to principal faster than you can service it. Eventually the math asserts itself, not dramatically but incrementally, through rising costs, reduced flexibility, and the gradual foreclosure of options that once seemed available. Interest payments consume a larger share of the budget. The capacity to respond to future emergencies shrinks. The feedback loop tightens.

History is consistent on this point. Fiscal crises rarely arrive as sudden ruptures. They arrive as the accumulated consequence of years of choices that each seemed, individually, defensible. Against that backdrop, the occasional appearance of something resembling fiscal seriousness is worth examining, not as a model to be uncritically adopted, but as evidence that the alternative is not simply theoretical.

Zohran Mamdani’s recently unveiled $124.7 billion executive budget attempted to close significant financial gaps without defaulting to either widespread service elimination or dramatic tax increases. Specific elements of the plan drew legitimate criticism. But the underlying orientation, that responsible governance requires precision rather than ideology, and that the choice between fiscal discipline and human investment is frequently a false one, represented a kind of political seriousness that has become genuinely scarce at the national level.

Mamdani cannot seek the presidency. But the questions his approach raises are not parochial. What would it look like to have that orientation applied to the federal budget? What would a contemporary version of the Kasich-era deficit reduction effort look like, built for a political environment defined by polarization rather than the relative comity of the 1990s? These are not nostalgic questions. They are practical ones, because the conditions that made the late-1990s surpluses possible, compromise, prioritization, and the willingness to absorb political costs for long-term gains, were not historical accidents. They were choices. They can, in principle, be made again.

The 2026 midterms will shape the composition of the Congress that will have to eventually reckon with these questions. The 2028 presidential election will determine whether the country produces a leader willing to make fiscal stewardship a defining national priority rather than a talking point deployed selectively when it is politically convenient.

America does not need a figure who replicates Perot’s style. The bluntness, the charts, the third-party insurgency, those were products of a specific moment. What it may need is something closer to Perot’s underlying conviction: that there is a point at which the gap between what a government spends and what it takes in stops being a political problem and becomes a structural one, resistant to the usual tools of management and messaging.

That point is not hypothetical. It has a tendency to arrive before the people responsible for avoiding it have decided they are ready to take it seriously. Every nation eventually reaches the same crossroads. Either it governs its debt, or its debt begins governing it.

The United States is not yet at the point of no return. But the window for serious action is not unlimited, and the political class has spent several decades demonstrating a remarkable capacity for treating urgency as someone else’s problem. Whether that changes before the math forces it to may be the defining question of the decade ahead.